In the U.S. this year, men and women will start more than 400,000 new businesses. Over the next five years, many of these businesses will flourish. Some will be acquired. Some of the owners will determine the business wasn’t what they thought it would be and will choose to close it. Some of the businesses will fail and the owner will be forced to close it.

One of the most vexing challenges facing those who run small businesses or the companies that serve them is this: What makes a small business last? Is there a way to determine those who will likely make it, from those that won’t?

In an effort to understand what separates businesses that continue to operate five years or longer from those that don’t, Sage, the software company, has conducted a survey of four different groups of business owners and advisors for its “State of the Startup, 2015 (PDF)” report being released today:

- 175 companies founded within the past 12 months

- 175 companies that are between 1 and 2 years old

- 174 companies that are between 3 and 5 years old

- 102 senior executives at companies who routinely nurture new business startups (accountants, business bankers, attorneys, seed and venture investors, incubators, business owner groups)

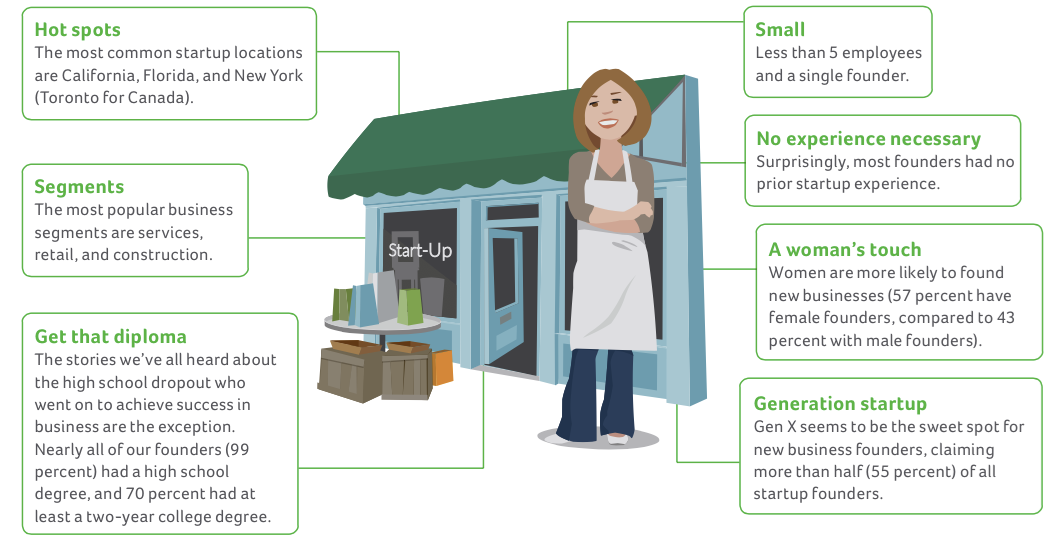

Snapshot of a typical business that has recently started

Click image for larger view

What is success?

There are many ways to survive to year five, so Sage focused on a specific set of metrics in order to make a comparison of the 524 business owners they surveyed. They focused on these:

- Growth of top-line revenue

- Profitability

- Hiring status

- Confidence in the business financials they produce

- Awareness of their company among their prospective clients or customers

- When they started to take a paycheck

- How they are doing in terms of meeting their original goals

What are the characteristics of a successful business less than five years old?

Using those criteria, the researchers compared the top-tier startups (those that scored highest using the metrics) against the bottom-tier startups, to analyze the differences in business practices and discover any secrets of the top tier. Here are what they found:

- They are more likely owned by partners

- They more likely had a business plan before starting

- They more likely hired professional advisors

- They more likely embrace new forms of marketing

- They more likely have a balanced life that’s not “all work”

Advice from long time small business observers

SmallBusiness.com spoke with Connie Certusi, the executive vice president and general manager of Sage Small Business Solutions, to see if there were any common threads running through the stories of those companies that make it through the five years. Certusi has worked with the small business software products at Sage for more than two decades (some may recall the previous brand, Peachtree). She and several other Sage veterans combined their expertise and the insights provided in the in-depth study and came up with this list of recommendations that can improve the odds for success for founders of new businesses:

No experience? No problem!

Do not let the fact you may not have experience in starting a business or running a team at a large company discourage you and prevent you from trying. Not only did most of our survey respondents have no prior startup experience, but neither did their parents.

Don’t wing it; have a plan.

One of the first steps for a significant majority of successful entrepreneurs was to create a formal business plan. Doing so helps answer questions you may have for yourself and even come up with new ones you haven’t thought of yet, such as whether you should have a partner. A business plan is also an absolute requirement if you plan to approach a bank, a venture capitalist or any other potential funding sources.

Do your research.

Conduct a thorough market analysis: Who are your target customers, your competitors? What trends can you take advantage of? This information can help you set specific objectives that you want to achieve over the course of the first year. Each of those objectives should be built around a narrative and specific numbers you are aiming for, such as revenue and market share.

Hire a trusted advisor.

To succeed, you need to make money. To make money, you need to attract new customers. You also need a clear and up-to- date understanding of how much money you’re making, where it’s coming in from, and where it is going. An accountant can not only help with financials, but they can advise you on other business decisions.

Seek opportunities to network.

Attend events and educational seminars to increase your knowledge, discuss new concepts, and exchange ideas with your peers. Meet people who share your perspective or who may show you a new one. You may discover how to optimize your business management processes or build your company’s value. Both the education and the networking will pay dividends.

Don’t be afraid to break the rules.

Entrepreneurs often have to forge their own path, take the road less traveled and do it their own way. Sometimes it’s necessary to break the rules to grow and succeed.